{kind=link}

Only 10% of investors making profits has long become a familiar figure in the stock market. In a conference earlier this year, the leaders of Dragon Capital cited a statistic indicating that over 90% of investor accounts are either not profitable or have profits below 10%. The number of accounts recording profits above 20%, which is equivalent to or exceeds the increase of the VN-Index, is very small.

In reality, the boundary between success and failure in the market is not only reflected in the numbers on the electronic board but also lies deep within the folds of the human brain. During a seminar last weekend, Mr. Nguyễn An Huy – Director of Wealth Management Hub Đồng hành of FIDT – referenced research by Daniel Kahneman – a psychologist who won the Nobel Prize in Economics in 2002 – showing that behavioral psychology greatly influences each person’s investment process. Contrary to the assumption of a “rational human” who always maintains alertness and logic, many investors are “systematically irrational”.

Research indicates that many mistakes in life, including investing, often stem from the conflict between two thinking systems: System 1 (fast, automatic, emotional thinking) and System 2 (slow, analytical, logical thinking). In most daily decisions, System 1 dominates due to its ability to process instantly based on experience and heuristics. However, this quickness creates biases when applied to the complex financial environment.

One of the most common barriers is confirmation bias. Instead of analyzing objectively to make decisions, most investors tend to decide first by intuition, and then seek evidence to support that choice. This phenomenon causes many to ignore contradictory information, and even when faced with counter-evidence, their belief in the initial mistake becomes even stronger. This leads to a loop: decisions based on desire, followed by an unconscious search for and acceptance of information to reassure themselves that they are right.

Additionally, hindsight bias often appears after an event has occurred, causing investors to mistakenly believe they had predicted the outcome beforehand. Familiar phrases like “I knew the market would crash” or “the signs were too clear” are actually a form of illusion created by the brain to create a sense of control over a random world. This feeling leads investors to believe that they can accurately control or respond to market fluctuations that have already been reflected in prices.

Especially, according to Mr. An Huy’s research, aversion to ambiguity is currently the strongest bias in the psychology of Vietnamese investors. He explains that many people are not afraid of risk if they know the probabilities, and conversely: they are extremely fearful of what is unclear. This bias narrows the investment portfolio to familiar channels and causes them to completely close off to new opportunities simply because they do not “feel” the rules governing them.

Experts believe that if emotional decision-making mistakes are avoided, the success rate of investors will increase. This is similar to the saying of Charlie Munger – Vice Chairman of Berkshire Hathaway, the conglomerate controlled by Warren Buffett: “Everyone tries to appear smart, while I just try not to be stupid, but that is harder than most people think.”

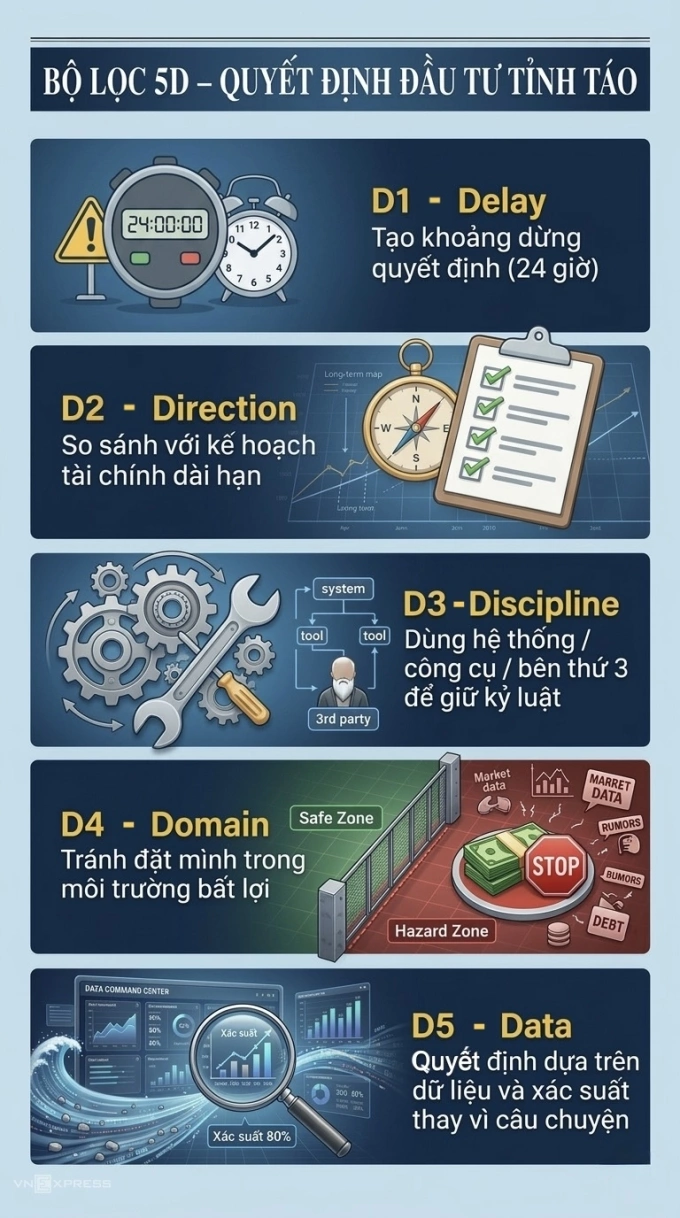

To begin the process of control, according to experts, the first and most important step is to “name” the biases, understanding how they operate in the subconscious. Scientific studies show that it is impossible to completely turn off System 1 or erase all biases. Therefore, the way to overcome them is to practice “slowing down” to “bring” System 2 into play.

Cultivating the habit of reading books instead of scrolling through short content on social media is an effective way to escape the quick thinking rut. At the same time, “meditation” (in a neuroscience sense) is also recommended as a tool to observe one’s own thoughts, helping to create the necessary pause before hitting the trade button.

A more practical strategy is to use tools instead of relying on willpower. Investors need to establish strict principles and delegate execution to a third party or an automated system to avoid being influenced by momentary emotions. For example, to combat loss aversion, a pre-established filtering system or long-term financial plan will serve as an “objective measure,” helping to make decisions based on numbers rather than feelings.

In many fields, experience is a valuable asset that enhances skills. However, in the stock market, experience can sometimes be a “double-edged sword.” A wrong decision that yields the right result due to luck can lead investors to become overly confident, resulting in failure in subsequent attempts.

To combine experience wisely, Mr. An Huy advises investors to learn to distinguish between results that come from ability and those that come from luck. Each time they achieve a victory, they should pause to analyze which factors truly contributed to that success. Looking at the failure lessons of others instead of only focusing on successful examples (survivorship bias) will help build a more comprehensive and realistic picture.

“Seeking evidence against one’s own argument (falsification) is the most effective way to verify the true value of experience,” he emphasizes.

Before each important decision, investors can self-question through three questions: What financial goal does this decision serve? Where might my investment argument be wrong? If this investment drops by 30%, what will I do?